Inflation Data Hot, Yields Rise, While Equities Put in Another High

Market Wrap

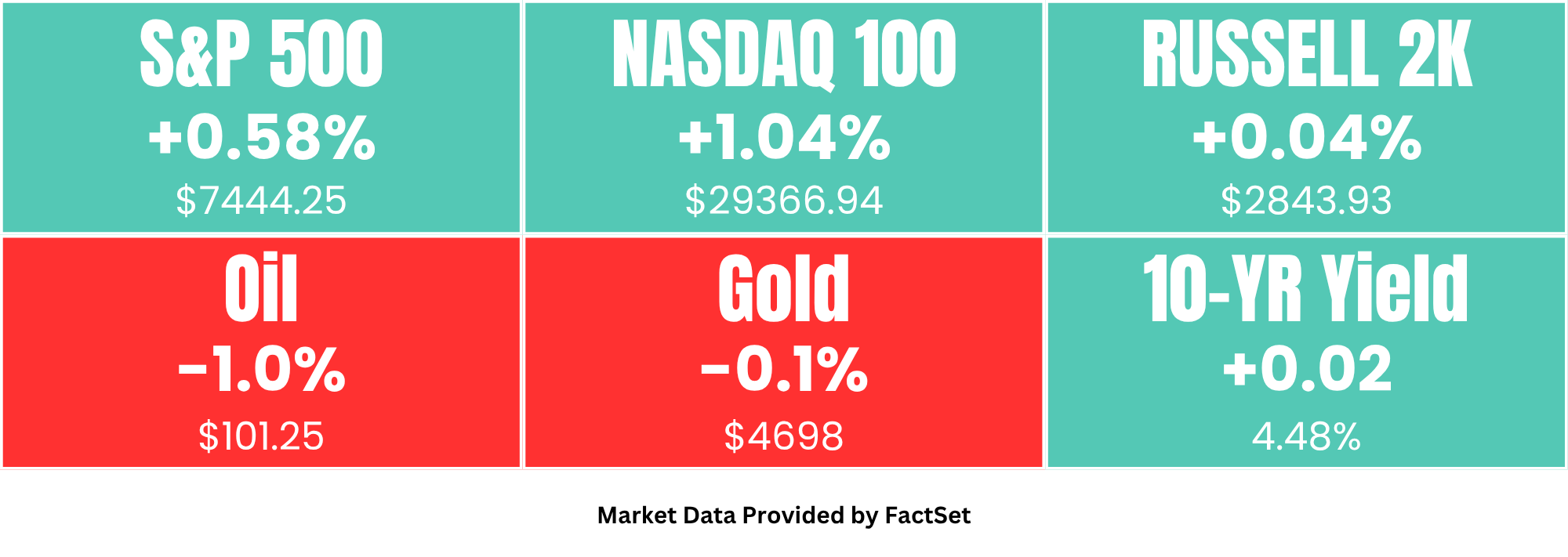

Another new SPX and NDX high

NVDA surging into earnings

Inflation data gets even hotter, yields rising towards multi year highs

The market continued to shrug off warnings from inflation data, rising yields, and stubbornly high oil prices, with the major indices once again pushing to fresh all-time highs. The story remains largely the same: tech continues to lead, even as there are some mixed moves beneath the surface. NVDA continues to charge higher into its report next week.

Outside of equities, the biggest story this week — beyond oil reclaiming $100 — has been yields. Not only are they moving higher alongside crude, but they’re also reacting to the hotter inflation data from the past two days, which has all but erased hopes for rate cuts and even revived some chatter about potential hikes later this year if conditions don’t improve.

The US10YY is now up to 4.48%, and a move back above 4.50% for the first time in roughly a year is increasingly in play. The 30YY is also approaching multi-year highs.

Oil eased slightly today but still looks likely to remain around the $100 area for the time being, now near $101. And we’re already beginning to see the impact show up in the data, with today’s PPI print the hottest since 2022.

The VIX was slightly lower on the day, back below 18, though it still feels somewhat stubborn considering the market continues to make new highs. At this point it’s likely pricing a combination of upside momentum in tech alongside lingering oil and rates risk. It’s worth watching if the VIX starts creeping back toward 20 even while equities remain near highs.

The dollar was slightly higher again, with DXY now around 98.50, while Gold continues to hover near the 4700 level.

Sector-wise, today was once again all about tech. NVDA continues to surge into next week’s report, making another all-time high after already gaining nearly +14% in May and now more than +20% on the year. As a reminder, NVDA had essentially gone sideways for the better part of 8–9 months (before this recent breakout) as other semi names surged.

The continued strength in semis has come somewhat at the expense of software lately. IGV is basically unchanged over the past three weeks even as the Nasdaq keeps pushing higher. To the downside, Financials stood out again. XLF is still negative on the year and essentially flat dating back to late 2024.

After Hours:

Today’s MRKT Call: Trump Flies to China. Jensen’s on the Plane. Taiwan Might Be the Price.

Today’s RiskReversal Pod: The $400 Billion Backlog: RBC’s Top Analysts Break Down The AI Trade

Listen to the MRKT MATRIX summary of today’s top stories:

Articles Mentioned:

S&P 500 hits another record driven by tech alone as most stocks decline on the day (CNBC)

Wholesale inflation jumps 6% in April on annual basis, biggest increase since 2022 (CNBC)

Wall Street Is Getting More Anxious About Long-Term Inflation (WSJ)

Treasury Buyers Get 5% Long Bond for First Time Since 2007 (Bloomberg)

Kevin Warsh Is Confirmed as Fed Chair in 54–45 Senate Vote (WSJ)

What Trump and Xi Want to Achieve at Their High-Stakes Summit (WSJ)

Alibaba jumps as it strikes bullish tone on AI investments, even as profit plunges (CNBC)

What’s next?

Looking ahead, we’re now past the inflation data, which the market largely ignored, but it may not be something traders can dismiss forever. Oil still looks like it will stay stubbornly high, and that only adds more pressure to this week’s inflation readings that were reminiscent of parts of the post-COVID inflation cycle. As a reminder, that environment eventually led to a year-long bear market. That doesn’t mean this setup has to play out the same way, but yields may become increasingly important soon.

Tomorrow, attention shifts toward any headlines coming out of the China meetings, along with what could be a very interesting Retail Sales number in the morning. On the earnings side, AMAT after the close could also be important for the broader AI and semiconductor trade.

Short-duration vol remains subdued, which continues to encourage the buy-the-dip behavior we’ve seen lately. Breadth is increasingly becoming an issue as the market is driven more and more by semiconductor names each day. That’s worth watching closely, because if that trade pauses or rolls over even temporarily, it could leave the broader indices exposed to at least a quick pullback.

Thursday, May 14th

Pre-market - ONDS 11%

US/China Summit

8:30am - Retail Sales

8:30am - Initial Jobless Claims

Fed Speak - Schmid, Williams, Barr, Hammack

After-hours - AMAT 8%, NU 7%

SPX Expected Move: 0.5%

Watch Today’s MRKT Call: Trump Flies to China. Jensen’s on the Plane. Taiwan Might Be the Price.

Dan and Guy on hot inflation and when that becomes a problem in yields and then eventually stocks. How pressure on the fed to cut rates won’t happen now. The China/US summit and battles over AI models, chips and more. Inflation and the consumer and what to look for as the big box stores report. Also looking ahead to NVDA earnings next week.

Analysis - SPX, NDX, US30YY, NVDA, TSM, COF, HD, NKE, LOW, COST, WMT, MU, NVDA

Learn more about our sponsors, Nasdaq and FactSet.

Watch Today’s RiskReversal Pod: The $400 Billion Backlog: RBC’s Top Analysts Break Down The AI Trade

At RBC Capital Markets’ Private Tech Conference, Dan interviews RBC analysts Brad Erickson, Rishi Jaluria, Matt Swanson, and Matt Hedberg on Q1 earnings and AI’s impact across internet and software. Erickson says demand is solid, hyperscalers are raising CapEx as cloud ROI improves, and explains why Meta’s higher spend hurt the stock versus Google/Amazon’s accelerating cloud revenue and margins; he ranks Amazon over Google over Meta and discusses Uber’s AV positioning versus Waymo. Jaluria is bullish on Microsoft’s broad AI opportunities, notes Copilot’s growing paid users, and discusses multimodel strategy, small/medium models, and Oracle’s controversial OpenAI-linked data center build and financing. Swanson covers ad/martech, highlighting Adobe’s “orchestration” narrative, Trade Desk’s holding-company tensions, and AppLovin’s ROAS-driven model. Hedberg argues cyber and infrastructure need “more, not less” security post-Anthropic’s Mythos, cites capitulation in software sentiment, favors consolidators like CrowdStrike, Palo Alto, Snowflake, Datadog, and ServiceNow, and notes AI-driven efficiency and layoffs as potential catalysts amid continued volatility.

Learn more about our sponsors, RBC Capital and Current.

Anthony Scaramucci at Hunt & Fish Club Restaurant | Standing Table Episode #1

Learn more about our sponsor Apex Fintech Solutions